Many real estate investors are curious about the true costs of building ground-up duplexes or triplexes. These properties offer a unique middle ground—more autonomy than a large apartment complex, yet more efficiency than multiple single-family homes. With small multifamily properties making up only about 6% of the market nationwide, limited inventory and consistent demand are pushing more investors to consider new construction.

Small multifamily, in this context, refers to buildings with fewer than four residential units under one roof. There are two primary construction styles: unit-over-unit and side-by-side. Within these categories, there’s plenty of room for architectural and layout variation. Each unit has its own exterior entrance, offering complete functional separation, although units do share a wall or a ceiling/floor.

Let’s break this big topic into manageable sections, and then take a closer look at each—using a real-world example from our multifamily project in Columbus, Ohio.

Financial Analysis

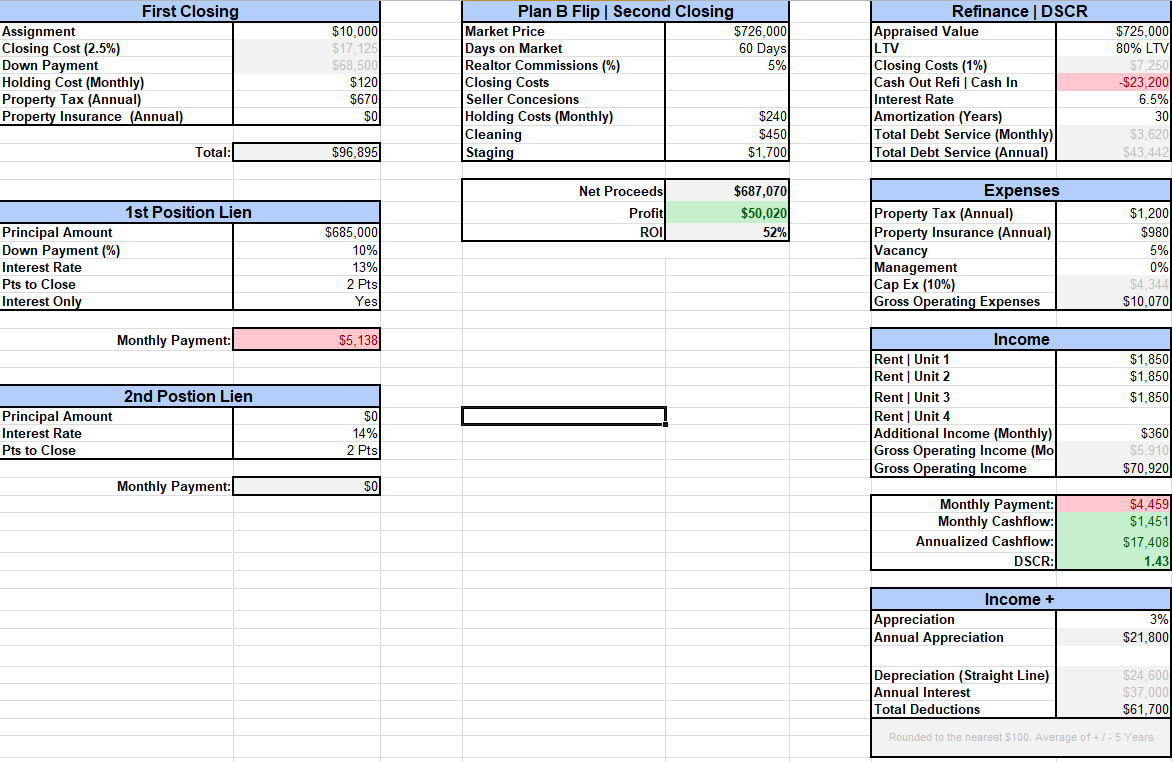

Financial analysis is the critical first step to ensuring the profitability of a project. In addition to including analysis of our primary interest, which is to refinance the property into long term debt and keep it as a rental, we also include analysis of a flip scenario. Should anything cause our costs to rise during construction, a solid Plan B helps ensure the interests of stakeholders. Protect your stakeholders.

Construction Costs

Just like any construction project, the cost to build varies depending on location, materials, and size. The national average cost to build small multifamily properties is $130 per square foot.

Land

It’s important to note that land acquisition costs are separate from construction costs.

Valuation

Valuation for small multifamily projects (less than 4 units) will be based on comparable sales.

Financing

For this project, we’re working with a private lender.

Let’s jump right in.

Financial Analysis

While our construction is expected to take 150 days, we anticipate 12-18 months from start to finish. By finished, we mean that tenants are in place, we’ve refinanced and transitioned into our long term debt and our short term financing is returned.

We’ll need to account for the transactional costs of financing, interest rates, raw land purchase, clearing and grading of the lot if necessary, construction draws and a mouthful of other variables we can share in the attached workbook.

While our intention is to refinance and keep this property as a rental, we’ll also include a look at a Plan B, in the event our appraisal comes in short and our refinance is going to be fuzzy. In this scenario, we’ll look at the implications of marketing and selling the property to hedge against the potential of loss to our stakeholders.

For more information regarding determining the net proceeds from a sale check out our article How to Determine Net Proceeds from a Sale.

At the time of writing this, we don’t know our exact costs of construction. We have a proforma breakdown of our unit size and market rent and a price per sq ft. This price does not include the land and includes all our soft cost: architectural plans, slight cosmetic modifications to the exterior finishes, re-entitlement, building permits and surveying and engineering costs. We we’re fortunate to not be clearing land or changing grading and our access to utilities is available near street.

While there’s a ton of variables, the focal point of our analysis is the DSCR. Anything above a 1.25 suggests that, assuming we’re not grossly negligible, the property will support itself.

Feel free to take a look at our financial analysis below.

Construction Costs

Layout has the single largest impact on the overall building cost. In general, unit-over-unit structures are the most cost-efficient to build, because they require smaller roofs, foundations and offer the potential to centralize plumbing and wiring.

Side-by-side dwellings tend to be more expensive, thanks to a bigger foundational footprint, larger roofs and additional plumbing and electrical lines.

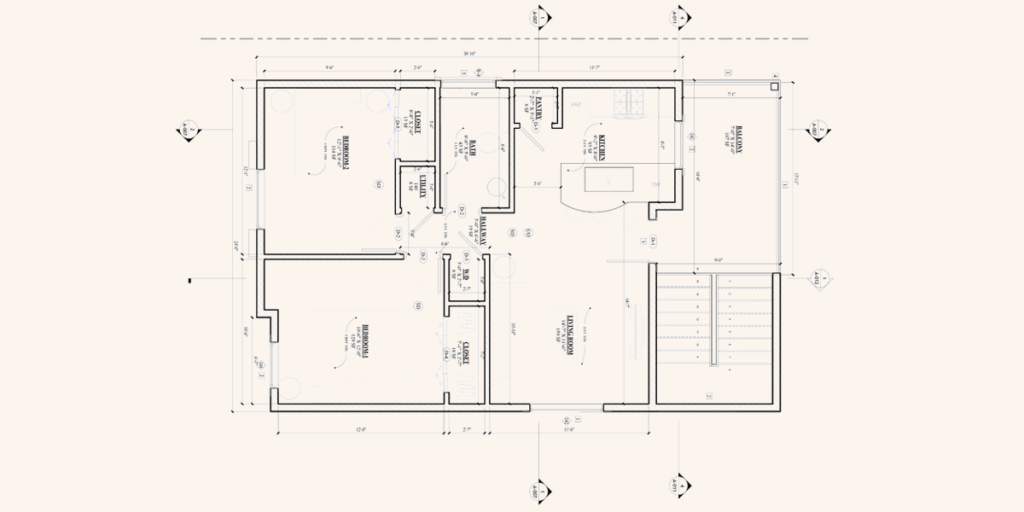

We’re opting for a vertical triplex with three 1,100 sq ft units, 2 bedrooms and 2 baths. With total sq footage around 3,300 our construction bid needs to come in around $165 sq ft. At the time of writing this article, we’ve received a bid of $190 per square foot and we’re working with a second builder to see how close we can get to $165 per square foot.

Land

Land prices are probably the most variable cost in the entire project, ranging by geography from a few thousand dollars to millions of dollars for infill lots in urban areas.

Undeveloped lots will require additional costs to bring in utilities.

Instead of closing on the land before we know if the cost is prohibitive to build, we’re using a 3 month option. The cost of the option is applied towards the purchase price of the land after due diligence is complete. At the recommendation of the builder, we’ve included an additional extension of 3 months, in the event the entitlement process takes longer than expected.

Zoning is another important factor to keep in mind when considering a location. While many municipalities will offer options to re-entitle land, not all areas are zoned for multi-family dwellings.

Our primary focus, when selecting an ideal lot is proximity to amenities that tenants will enjoy and comparable sales. Ensuring the project reaches its anticipated valuation (after 6 months of seasoning), plays a significant role in the viability of the long term debt compared to income and overall feasibility of the project. We’re lucky to have 5-6 great comparable sales in the area.

Valuation

As built value is as much an art as it is a science. With 5-6 great comparable sales nearby, there’s a high probability of our as-built value being sufficient to cash out refinance at 6 months with 80% LTV and allow us to not leave a huge chunk of cash in the deal.

One really important consideration for our project is ensuring the seasoning period starts at the commencement of construction and not once complete. Few lenders offer such and it can have a significant baring on the high cost of short term debt, so its a a good thing to take into consideration when choosing a lender.

Financing

Please see the above workbook.

Conclusion

Triplexes are a great way to get your feet wet in new construction. A solid team of partners with a track record of excellence make the difference between paralysis and practical steps forward.